Split sentiment

The report signalled a sense of optimism amongst panellists regarding their own company's financial prospects as 7.0% of firms were optimistic towards their business outlook up significantly from -17.2% previously. However at industry level, many remain pessimistic.

Yet while Bellwether panel remembers are cautious in their approach to the financial climate, a proportion had grown more confident. With 22.8% of companies downbeat in their assessment compared to 41.8% previously, the numbers of optimists seemingly grow meaning that this report signals the weakest degree of negativity in a year.

“This is a positive start to the financial year for marketing budgets, all things considered, The overall increase in confidence from UK companies regarding their financial prospects is being reflected in their marketing budget decision making.” commented Paul Bainsfair, IPA Director General.

Putting plans into action

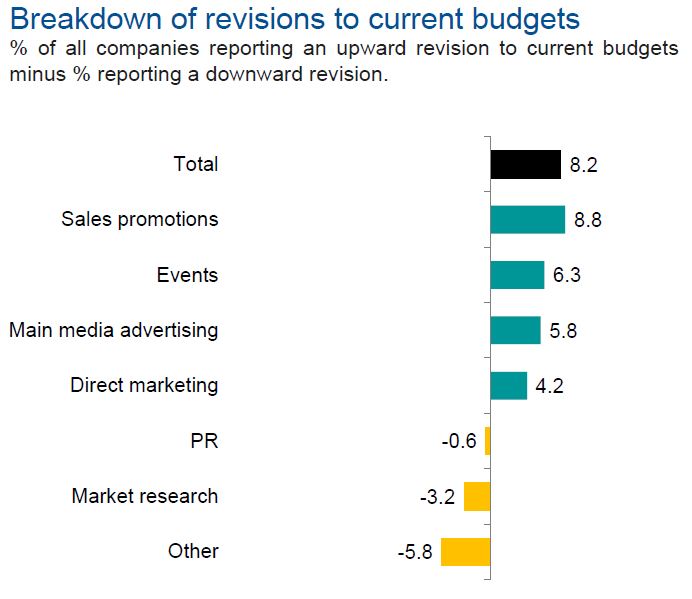

Budget plans for 2023/24 are indicative of this cautiously optimistic approach. Expectations towards marketing budgets for the new financial year were strongly positive in line with previous estimations. More than a third (36.6%) of respondents foresee greater total marketing spend in real terms in the year ahead, compared with 16.9% anticipating cuts.

Category growth is set to be expected in face-to-face marketing activities such as events which is predicted to see growth of +14.5%. Where post-pandemic the events industry has proved the value of human interaction, maximising on the benefits of face-to-face connection holds strong appeal for both brands and consumers.

Main media budgets and sales promotions budgets are also set to rise showing that brands are settling into a cost-of-living crisis with no near end in sight.

“As the cost-of-living crisis continues, it is understandable for companies to offer sales promotions to help their customers’ tightened purse strings. To ensure brand loyalty isn’t eroded and to protect the long-term health of their brands, however, such activity must be coupled with investment in longer-term brand-building media.” added Bainsfair.

Looking long-term

Beyond 2024 the report forecasts adspend to improve. S&P Global’s forecast for the UK economy has been modestly upgraded, with GDP in 2023 expected to decline by -0.2%, instead of the -0.8% anticipated in the last Bellwether Report.

However, households continue to face shrinking purchasing power due to high inflation and borrowing costs, which the report suggests is set to weigh heavily on the economy. In response to this Bellwether has issued a revised forecast, which predicts a small decline of -0.9% (vs. -0.3% previously) in adspend this year, a marginal improvement in adspend next year of 0.5%, before expected growth to 1.6%, 2.0% and 2.2% in 2025, 2026 and 2027 respectively.

For marketers and decision-makers, the report signifies a clear small but stable growth opportunity. While proceeding with caution is advised, the industry holds a strong position in its ability to weather economic headwinds as marketing efforts prove vital in helping both brands and consumers through the ongoing cost of living crisis.